I have been quiet for some time due to personal reasons, but I haven’t stopped buying in the market. Moving around during the pandemic sure is fun, but the pain of moving is excruciating. Currently I’m living beautiful British Columbia.

Investment Update

But just a quick update on where I am – in the past 2 months, I have increased my position in Frontera Energy by 25% and increased my position in Petrotal by 1.8%. Currently, Frontera and Petrotal offers significant upside, due Frontera’s Guyana exploration program, and Petrotal’s social unrest, and production increase.

PTAL Catalysts

- 9H

- ONP reopening

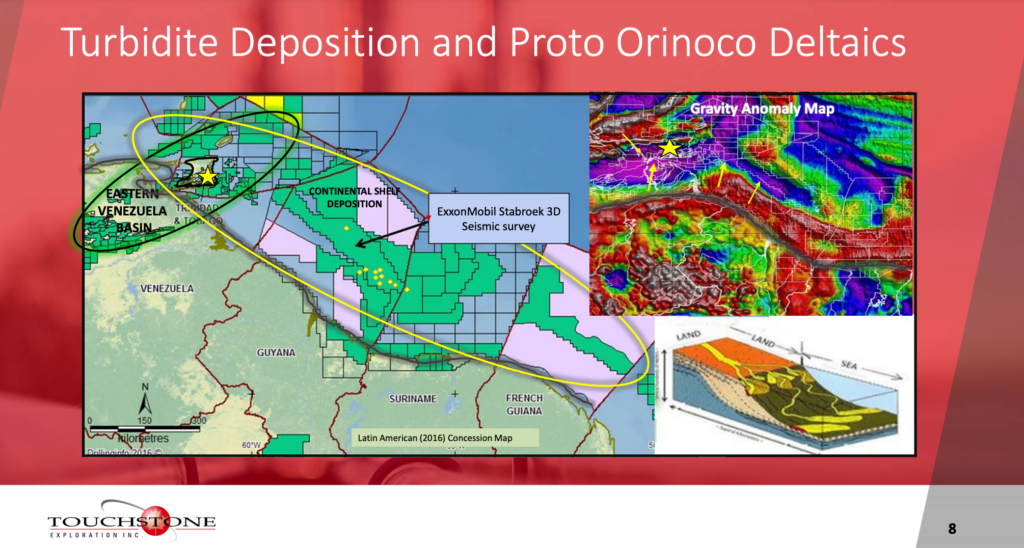

FEC Catalyst

- Dividend reinstatement

- Puerto Bahia

- Kawa-1 results

- Colombia exploration and production increase

- NCIB

While I’m preparing to get back to more blogging, I’m anxiously waiting for Frontera’s Kawa-1 well results, and Petrotal’s 9H Completion. Exciting times ahead!

My RSUs just unvested, so I have plenty of liquidity to purchase more. We are just in the beginning of O&G Bull Market.